The issue of reducing the water and carbon footprint is becoming a focal point in environmental management. Most large companies with agricultural value chains*, such as Coca Cola, Kellogg, General Mills, LVMH, etc., have developed supplier programmes that not only improve yields at a farm level but also drive their ‘own’ environmental sustainability focus. By engaging actors along a value chain, stakeholders can exert influence on each other in shaping the behaviour towards a common goal of the sustainable use of natural resources.

In South Africa, the concept of value chain-based environmental management has gained support over the last couple of years. Through engagement with stakeholders along the sugar value chain, beverage manufacturers (Coca Cola, through the Amalgamated Beverage Industries [ABI]**) and the sugar milling companies have made headway towards achieving their environmental sustainability goals (greenhouse gas emissions, water use, etc.). An example is Illovo Sugar, which has consistently been among the best performing companies on the Johannesburg Stock Exchange*** Socially Responsible Investment (SRI) Index. The indicators used in the SRI Index fall into three broad categories: Environment, Society and Governance, and related sustainability concerns.

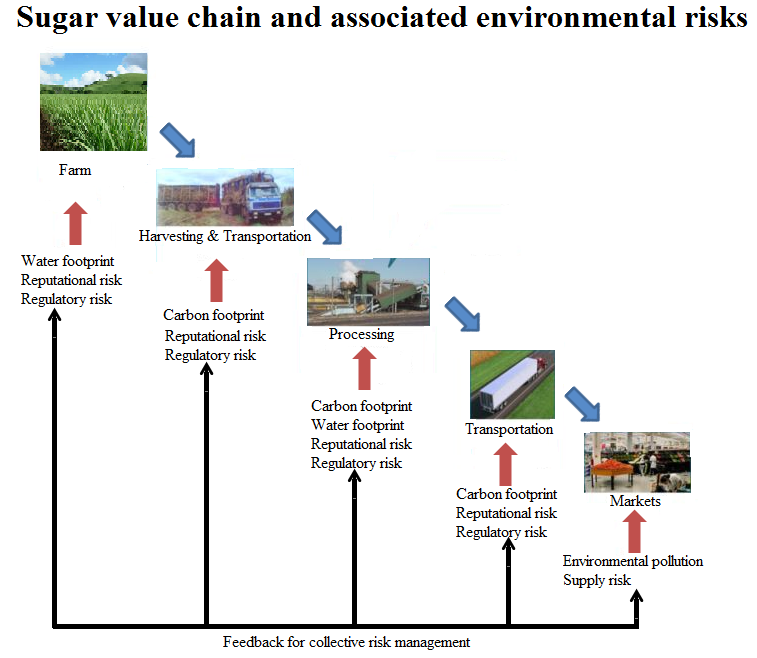

A value chain-based approach to environmental management has a number of advantages in terms of risk management, behaviour adjustment, activity specific interventions, and response diversity among others. A case study of water security in the South African sugar industry carried out at Monash South Africa has shown that this approach leads to an alignment of behaviour. Through the local Mill Group Boards – a platform in which sugarcane growers and sugar mill representatives participate – rules dictating the best farming practices and the delivery of sugarcane to the sugar mills can be set. This collective formulation of rules sets the tone for collective action towards the sustainable use of natural resources. What motivates the growers to participate in the Mill Group Boards is the competitive desire to maintain access to the next link in their value chain – the mills. For the sugar mills, more efficient and environmentally sensitive delivery of feedstock cuts costs and eases access to downstream markets.

In addition, a value chain-based approach allows for an ‘activity specific’ intervention, especially when coupled with programmes such as water footprinting (as has been done by Illovo Sugar across its operations in South Africa and the rest of Africa). An analysis of water use and/or requirements amongst actors along the value chain will give a general indication of where specific proactive interventions are needed in order to get to a state of sustainable use of natural resources. And the existence of value chain-embedded institutions such as the SRI Index and the Mill Group Boards provides an entry point for such new information into the sector.

Furthermore, this approach opens up actors to diverse response mechanisms from other stakeholders in managing risks that may affect them, thus allowing for comprehensive risk management. This fosters a sense of esprit de corps. This can be seen with the Sustainable Sugarcane Farm Management System (SUSFARMS®). Collaboration along the sugar value chain has seen the development of the ‘SUSFARMS® 2018’ initiative, which drives the environmental sustainability goals of stakeholders. The initiative gives the sugarcane growers and millers an opportunity to brand their farm produce as ‘produced in an environmentally friendly’ manner whilst the beverage manufacturers can fulfill their ‘responsible material sourcing’ goals, thus contributing to their financial sustainability as stakeholders in the sugar value chain.

Despite the advantages that can accrue from adopting a value chain-based approach, a lack of coordination in environmental management has always led to a duplication of roles and, often, cross-purpose working among stakeholders. This then brings to the fore a number of questions: does the value chain concept have space in the water sector? If so, to what extend should the value chain approach be used for mainstream environmental management issues, such as water management?

* A value chain describes the full range of activities which are required to bring a product or service from conception, through the different phases of production (involving a combination of physical transformation and the input of various producer services), delivery to final consumers, and final disposal after use (Raphael Kaplinsky, & Mike Morris, A handbook for value chain research (Vol. 113) (Ottawa: IDRC, 2001).

** ABI Bottling (Pty) Ltd is a franchised bottler of The Coca-Cola Company and a leading soft drinks business in the international SABMiller group of companies.

*** Illovo Sugar delisted from the Johannesburg Stock Exchange in June 2016 after Associated British Foods’ acquisition of Illovo minority interests.